Conjoncture économique

General overview

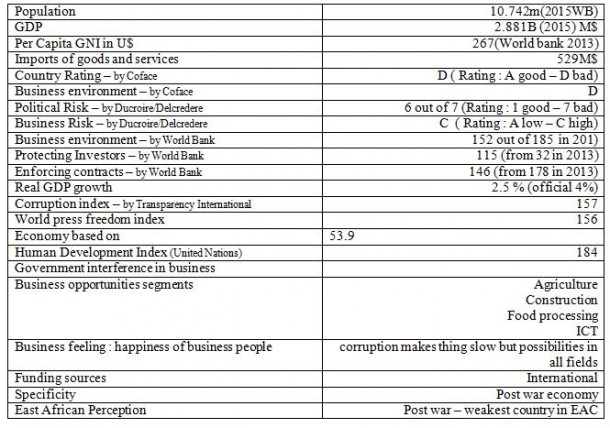

The Republic of Burundi is a landlocked country in the Great Lakes region of Eastern Africa bordered by Rwanda to the north, Tanzania to the east and south, and the Democratic Republic of the Congo to the west. Its size is just under 28,000 km² with an estimated population of almost 10.16M its capital is Bujumbura. Although the country is landlocked, much of the south-western border is adjacent to Lake Tanganyika.

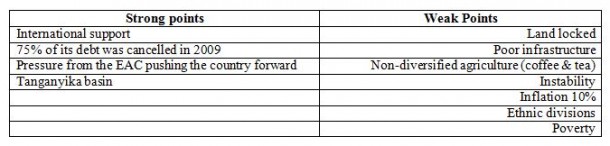

Burundi is recovering from a 15-year civil war in which 300,000 people died. The conflict ended with a peace agreement in 2008. Fighting began in 1993 when soldiers from the ethnic Tutsi minority assassinated the leader of the main party of the Hutu majority who had just won the first democratic presidential elections.

Burundi is one of the world's poorest countries, owing in part to its landlocked geography, poor legal and education systems, an increasing density of population which reduces the size of available land per household, and the proliferation of HIV/AIDS. GDP per capita estimated at 155.06 US$ for 2013 and more than two-thirds of the population lives below the poverty line

Burundi has earned the title of "most corrupt" country in the East African Community ranking 150 out of 175 in countries, according to the Corruption Perceptions Index 2015 published by Transparency International.

Despite political uncertainty, the Economist Intelligence Unit forecasts real GDP growth of 7% in 2015 driven by agricultural production and investment. Burundi’s annual economic growth rate is expected to stabilize at 5 percent between 2013 and 2015 as the East African country rebuilds after a civil war.

Economic policymakers in the government will come under increasing pressure from their EAC counterparts over the next two years to bring themselves up to regional standards, and it is believed that this pressure will bring positive results.

Economic and commercial evolution

Burundi's largest industry is agriculture with “subsistence agriculture” accounting for most of it. The nation's largest source of revenue is coffee and tea. Coffee sales account for two-thirds of Burundi’s exports and the industry 800,000 households. It is expected that the recent privatization of 13 coffee washing stations will have positive spill-over effects on the entire sector. Because interest from foreign investors was initially limited, the government has decided to reissue the invitations to bid at the end of the current coffee campaign.

The primary sector contracted by 2% in 2013, mainly due to the effects of rainfall on coffee production. The economy has slowly recovered over the past two years as services and the secondary sector have expanded, the latter having benefited from investment in industry, construction and public works.

Input & Output

- Exports: 96.6 million. World Rank 195 (2015);

- Export commodities: coffee, tea, sugar, cotton, hides;

- Export partners: Germany 12.3%, Pakistan 10.7,Congo 10.7, Uganda 8.1%, Sweden 7.8% US7.1%, Belgium 6.3% Rwanda 4.6%, France: 4.4% (2015);

- Imports: 815.1 million. World Rank 184;

- Imports commodities: capital goods, petroleum products, foodstuffs;

- Import partners: Kenya 15%, Saudi Arabia14%, Tanzania 8.3%, China 7.1%, India 4.9%, France 4% (2015);

- GDP: composition by sector: Agriculture 39.2%, Industry 18.1%, services 42.7%;

- Inflation: 5.6% (2015).

Tea is Burundi's second largest foreign exchange earner after coffee and supports some 300,000 smallholder farmers in a nation of nearly 10 million people.

In 2013, total earnings from the tea dropped to $20.8 million from $26.3 million in 2012, due to weaker global prices.

Other agriculture products include: cotton, maize, sorghum, sweet potatoes, bananas, manioc (tapioca), beef, milk, and hides. Agricultural production is expected to improve, although weather patterns are uncertain and production is vulnerable to erratic rain patterns. Economic growth may be driven by improved management of the coffee industry and rising foreign aid inflows to build infrastructure, according to IMF.

Other natural resources include uranium, nickel, cobalt, copper, and platinum. Recorded earnings from "other primary products", which include gold smuggled in from the DRC, will fall slightly, because although plenty of gold is still coming into Burundi, more and more of it is also being smuggled out of the country and going unrecorded.

The manufacturing sector is expected to continue on its modest growth path. It mainly concern assembly of imported components; public works construction, food processing, and light consumer goods such as blankets, shoes, and soap. Textile output has collapsed and energy shortages will continue to pose a significant problem.

It’s expected to see modest increases in the production of beer and household consumer goods. In its role as a regional trading hub, Bujumbura should benefit from continued stability, and further integration with the EAC will prompt growth in the wholesale and retail sectors.

Imports to Burundi typically exceed exports by roughly 400%, and there seems little prospect of this ratio altering significantly. Tea and coffee production volumes are expected to rise during 2011-12, but this will be offset partly by falls in the international price of the two commodities.

Increased global competition for markets, which is pushing down prices, and the introduction of the EAC common market, which is reducing regional tariff and non-tariff barriers, will mitigate the rise in import costs during the forecast period.

Burundi's services deficit is expected to widen slightly as increased trade volumes result in higher freight costs.

Falling international fuel prices in 2011, coupled with an increase in domestic food production, will contain inflation. However, robust demand in areas such as construction and continued growth in the money supply will prevent inflation from falling significantly (forecast of 8% in 2011 and 7% in 2012). Burundi’s inflation rate was the highest in the region averaging 9.7 by the end of 2013.

Lack of access to financial services is a severe problem for the majority of the population. Access to financial services is limited, reflecting the underdeveloped payments system. Based on data from 2007–08, only 2 percent of the total population has a bank account, and less than 0.5 percent use bank credit services. Consequently, cash transactions predominate, and payment instruments are physically exchanged. Moreover, most small and medium-size enterprises find it difficult to obtain credit, mainly because of lack of adequate information on the creditworthiness of prospective borrowers, the unavailability of real guarantees, and weak capacity of project preparation.

IMF reiterated that Burundi needed to boost its spending on infrastructure, speed up integration into the regional trade bloc East African Community and further reform its financial sector.

According to the newly established Burundi Investment Promotion Authority, US$457m was invested in the country in 2013.

Official Website: http://www.burundi-gov.bi/

Economies of the Eastern African Communities

In 2010, the EAC (composed of five countries, Kenya, Tanzania, Uganda, Rwanda & Burundi) launched its own common market for goods, labour and capital within the region, with the goal of a common currency and full political federation in 2015.

The idea of this document is to compare different sources of data and enable the Belgian business man to have a quick overview of the East African Community’s economies.

The 5 countries are classified by order: Kenya being the largest economy and Burundi the smallest.

Indicators:

The data is an overall approach on countries. In some economies like Kenya one will find that doing business in Nairobi is different from Mombasa or Kisumu.

The GNI consists of: the personal consumption expenditures, the gross private investment, the government consumption expenditures, the net income from assets abroad (net income receipts), and the gross exports of goods and services, after deducting two components: the gross imports of goods and services, and the indirect business taxes. The GNI is similar to the gross national product (GNP), except that in measuring the GNP one does not deduct the indirect business taxes.

Ducroire/Delcredere is Belgium's overseas export credit insurer. It insures and reinsures the political and commercial risks of trade transactions. Political risk index goes from 1 (good) to 7 (bad) and commercial risk from A (low risk) to C (high risk) www.ducroire.be

Coface is the French export Credit insurer. Its rating reflects the average risk of short-term non-payment for companies in this country. Seven families are used A1 to A4, B, C & D. A1 (Belgium) Steady economic environment, good payment record of companies, very weak default probability to D (Afghanistan): High risk profile of the economic and political environment, very bad payment record. http://www.cofacerating.fr

World Bank analysed 189 Economies: 1 Best (Singapore in 2015) – 189 worst (Eritrea in 2015)

Transparency international monitors corruption: 1 Best (Denmark, New Zealand Finland, Sweden) – 178 Worst (Somalia).

The World press freedom index monitors freedom of expression: 1 Best (Finland) – 13 (Belgium) – 180 worst (Eritrea)

The “Business feeling” is a subjective point of view: it’s how the foreign local business people perceive the day to day business processes and its general perspectives. It can be good, medium or low. For instance Rwanda has a good rating by World Bank but poor ratings by the credit export agencies and world press freedom index, with intrusive public institutions into the business environment resulting in “low business feeling” by the local community.

This information was compiled from different sources: World Bank, Coface, Ducroire, EIU, official web sites of the countries, Transparency international, World press freedom, African Economic Outlook, personal inputs and data found on websites.

Ivan Korsak

Attaché économique et commercial

AMBASSADE DE BELGIQUE

Limuru Road, Muthaïga, Nairobi

P.O. Box 30 461 Nairobi

nairobi@belemb.eu

nairobi@brusselsinvestexport.com

T +254 20 405 20 90

F +254 20 712 26 13

www.brussels-in-east-africa.com